[ad_1]

When individuals can take part within the monetary techniques, they’re higher in a position to begin and develop companies, spend money on their youngsters’s training, and take up monetary shocks.

Sub-Saharan Africa has a inhabitants with most lives being on the financial downstream, and almost definitely underdeveloped. The monetary inclusion gender hole and earnings hole persisting identical to in different continents, although increased in Sub-Saharan Africa. World Inhabitants estimates based mostly on the most recent estimates launched on June 21, 2017, by the United Nations, reveals Africa continues because the second largest continent with a inhabitants of 1,256,268,025 (16% of the inhabitants of the world) and by the top of January 2018, 40.2% residing in city areas.

The continent has the best fertility price of 4.7% (Oceania 2.4%, Asia 2.2%, Latin American and Caribbean 2.1%, Northern America 1.9% and Europe 1.6%) in comparison with the opposite continents with a yearly inhabitants price change (improve) of two.55% – the best amongst all continents. Most of its individuals (59.8%) have lived downstream (rural areas and villages) typically out of the mainstream financial system. Coverage focusing on might be tough in such eventualities, and figuring out individuals who lack entry to monetary and financial inclusion comes with an enormous monetary price in itself, although the profit in doing so outweighs the associated fee in mere numbers and requires dedication from leaders and managers of the respective economies. Coupled with a common phenomenon of non-perfect, untrusted, and in some instances non-existing information on the continent, that would make resolution making imperfect and information unreliable, affecting plans, insurance policies and the potencies to resolve said challenges or enhancing the financial and social fibre of nations.

The struggles of the financially excluded come from boundaries and causes as entry, social and cultural components, earnings, training and lots of doable lists of others. Monetary exclusion arguably is among the causes some financial insurance policies lack efficiency to successfully goal nicely on the citizenry with its ends in persistent poverty and inequality. Lack of entry to fundamental wants like an account both on the financial institution or cell cash may imply vital potentialities of alternatives untapped. Globally nations have realized the significance of reaching inclusive societies and helps efforts at maximizing monetary inclusion. Sub- Saharan Africa has made some strides over time in monetary and financial inclusion on this regard at particular person nation ranges.

Efforts ongoing in Ghana embrace a dedication to selling and prioritizing monetary inclusion. The nation made particular and concrete commitments to additional advance monetary inclusion underneath the “Maya Declaration“ since 2012 and has an formidable goal of reaching 75% Common monetary inclusiveness of its grownup inhabitants by 2020. Ghana presently has 58% of its grownup inhabitants accessing monetary providers and can be finalizing its Nationwide Monetary Inclusion Technique which is able to change into the guiding doc and reference for inclusive actions, stakeholder roles and duties spelt out for all.

Kenya, nevertheless, has earned international recognition in main the all others on this planet in cell cash account penetration, and with twelve different sub-Saharan African International locations following, researchers present. The speed at which African nations are projecting innovation expertise for digital monetary inclusion is spectacular. The nation has made large strides in its monetary inclusion commitments, particularly underneath the Maya Declaration.

There was some paradigm shift in Info and Communication Expertise and its significance which is being thought-about as an element of financial development. ICT has the flexibility to supply providers with minimal price, enhance innovation, and supply infrastructure for handy and simple to make use of providers, it could additionally present a path to entry many auxiliary monetary providers.

On the macro stage, digital innovation affect financial improvement and financial coverage effectiveness.The advantages ICT enabled monetary providers embrace the doable creation of employment- cell cash distributors, will increase in income receipts of presidency, helps companies productiveness (each personal and public), assist in price management and efficiencies, and Might contribute to rural improvement and governance: Governance and income mobilization efforts, particularly at native authorities ranges, could be enhanced by ICT which aids in general enchancment in company governance. Importantly, Innovation Expertise will help within the deepening of monetary inclusion both by entry, utilization, decreasing threat and enhancing high quality of providers, thus, per formulation for Monetary Inclusion (FI), thus, FI = (Unlocking Entry + Unlocking Utilization + High quality) – Threat.

Entry to monetary providers can generate financial activities-Subtle use of monetary providers even presents larger financial and social potentialities for the included. In Mexico, a analysis by Bruhn and Love revealed that, there have been enormous impacts within the financial system in Mexico, that’s, 7% improve in all earnings ranges (in the area people) when Banco Azteca had speedy openings of branches in over a thousand Grupo Elektra retail shops when in comparison with different communities that branches weren’t opened. Additionally the financial savings proportion by these households in the area people decreased by 6.6%, a state of affairs attributed to the truth that households have been in a position to rely much less on financial savings as a buffer towards earnings fluctuation when formal credit score turned obtainable.

Right here, it should be famous that by financial savings is inspired, the discount in financial savings by 6.6% means extra funds can relatively be channeled for investments into economically viable entities or providers. Because the cycle continues, and in refined use of monetary providers alongside the monetary providers worth chain, they might want to save nevertheless for different investments later. Comparable or much more constructive correlation is noticed if the medium of entry and utilization is thru progressive expertise.

Utilizing Digital Monetary Inclusion Methods in Humanitarian Providers

Regardless of the use and usefulness of monetary providers in crises conditions, monetary exclusion is especially acute amongst crisis-affected nations. 75% of adults residing in nations with humanitarian crises stays outdoors of the formal monetary system and wrestle to answer shocks and emergencies, construct up productive belongings, and spend money on well being, training, and enterprise.

Researchers proceed to indicate the expansion in acceptance of digital funds particularly by using cellphones. There may be rising proof supporting digital monetary inclusion. GSMA in its experiences revealed that there have been 93 nations between the intervals of 2006-2016 of with 271 cell cash working service suppliers which had registered over 400 million accounts globally. They provide some proof in some nations – which have been receiving humanitarian assistance- the place there’s rising acceptance of digital monetary inclusion by use of a telephone.

In Rwanda vital numbers of refugees used telephones for cell cash providers whiles some achieve this commercially for service charges. In Uganda, Refugee communities are famous to be used of cell cash service as per the report. This has necessitated MNO Orange Uganda, a telecommunication agency to develop cell cash service to refugee communities by constructing a communication tower to enhance entry and utilization of the providers. In Pakistan, one of many largest refugee communities- third largest- has the federal government utilizing cell cash for money transfers to refugees. The proof abounds and this requires humanitarian businesses to rethink and rethink digital inclusive monetary providers past the present numbers. In Lebanon (The biggest refugee neighborhood) these on humanitarian help makes use of ATM issued by assist organizations to entry their money transfers.

Sarah Bailey, nevertheless, noticed that humanitarian areas that have been receiving money transfers by cell cash may improve using sure providers however doesn’t robotically result in widespread or sustained uptake. Folks might choose to proceed utilizing casual monetary techniques which can be extra acquainted, accessible and worthwhile. Her research revealed that that, the supply of humanitarian e-transfers, even when mixed with coaching, was not adequate to allow the overwhelming majority of individuals to conduct cell cash transactions independently.

The findings are definitely acceptable within the quick run per our data. Nevertheless, on a long-term foundation and with monetary functionality actions – not simply training- the outcomes may presumably be totally different. Monetary functionality actions take care of not simply coaching and training, however the general monetary well being and well-being of the individuals. And this needs to be completed in a hierarchy- bits-by-bits- and never at a one leap leap method. This appears to have been echoed by the United Nations. In line with Ban Ki-moon as cited in suggested that we should return our focus to the individuals on the centre of those crises, shifting past short-term, supply-driven response efforts in direction of demand-driven outcomes that scale back want and vulnerability. Monetary inclusion methods might not result in widespread uptake inside a couple of days, however proof abounds that in a long-term, it may.

The 13 nations on this planet with probably the most cell cash penetration right now had some being on humanitarian help only a few years back-. Sustained entry and use of progressive expertise for inclusion then would have a greater impression on them the extra right now.

Endeavor a case research on using digital means for humanitarian switch will present that within the quick time period run there could also be lack of curiosity and even rejection. Coupled with regulatory boundaries and different boundaries talked about, individuals throughout a humanitarian disaster might not likely be pondering a lot of connecting to the financial system on the entire or how their help comes (That is the enterprise of policymakers on humanitarian service) however relatively be a lot considering survival inside a brief run. The psychology of that interval of want is centred on – What is required is the urgency of help – cash – bodily money normally to allow them to get the fundamentals of safety and meals with probably the most liquid instrument. Humanitarian communities have wants simply as all different communities throughout the monetary providers want a framework.

Certainly proof suggests there have been few situations solely worldwide the place using digital transfers in humanitarian transfers has led to widespread use of providers. Digital transfers in humanitarian providers should be a course of and completed throughout the explicit context of time. On this sense, the digital methods should be humanitarian, and should embed within the social and behavioural change monetary functionality actions able to two-way communications with practices on utilization and the advantages it brings within the lengthy term- It should be in a hierarchy. Easy monetary wants needs to be met earlier than refined wants. Any deviation will after all ends in lack of curiosity within the providers.

Howard Thomas noticed that “Monetary expertise nonetheless leaves out swathes of individuals, and this implies missed alternatives for improvement,” And in some instances, neighborhood constructions will not be progressive or agile sufficient to permit new applied sciences to unfold, he provides. “Savvy entrepreneurs usually are not essentially from established authorities. Typically it is a matter of figuring out particular person leaders, networks or pathways by which to advertise new applied sciences.”

Certainly there have been some classes nevertheless on easy methods to handle humanitarian remittance, the parameters, nevertheless, are that monetary inclusion is a steady and sustaining effort of offering entry and utilization of monetary providers in a sustaining and accountable method which meets the wants inside a decreased threat – it isn’t only one time undertaking of implementation insurance policies at pace however relatively think about assembly the essential earlier than refined wants. Inside a humanitarian sure, a fancy multiplicity of points might function boundaries to utilizing digital monetary providers together with location and pressing wants; nevertheless these boundaries when managed inside a substantial interval and matched with monetary functionality actions (the act of full monetary well-being), then beneficial outcomes could be achieved.

Using behavioural change monetary functionality training, coaching and apply into humanitarian communication on digital transfers would assist in enchancment within the uphill acceptance over a time frame. sub-Saharan African nations have been realizing some super features in using progressive expertise, and growth of ICT providers and infrastructure on the continent. Its research time previous factors out these nations on the continent completely made revenues amounting to five% of Gross Home Product (GDP) from telecommunication associated providers as in comparison with European nations the place revenues from the telecommunication providers represented 2.9% of their complete GDP.

Sub-Africans International locations want repositioning and additional funding within the “digital financial system” so as to open up and profit absolutely inclusiveness of their financial system. Right here our curiosity is in cell expertise and innovation which is the crucial avenue that Africa may use principally in reaching monetary inclusion throughout the quick to long run.

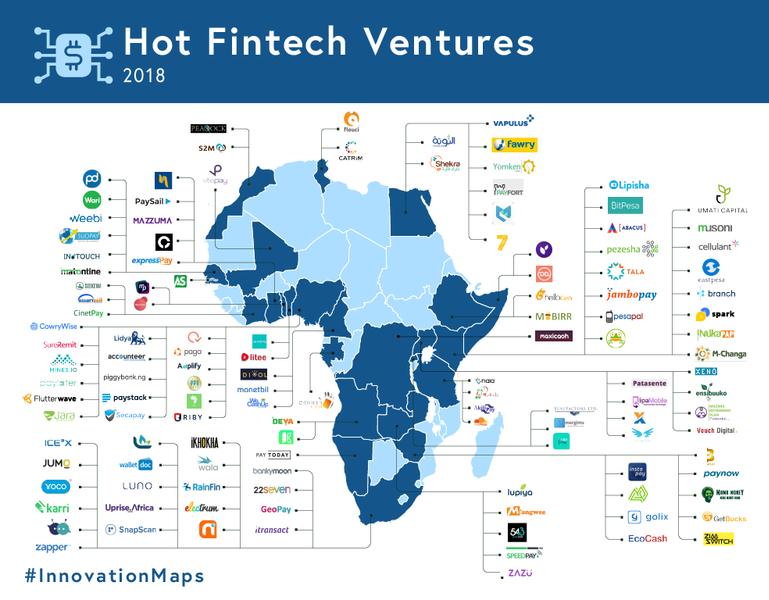

Kenya is making large strides and main the way in which in digital innovation for cell monetary providers globally. Researchers have proven that sub-Sahara Africa nations are main the technological innovation drive within the utilization of cell monetary providers.Kenya and different Sub-Saharan African nations are making the best strides in cell cash accounts penetration and with a number of alternatives foreseen. Globally the 13 nations that cell account penetration has been over 10 %, all 13 are from Africa -Botswana, Cote d’ivoire, Ghana, Mali, Kenya, Somalia, Rwanda, Namibia, Tanzania, South Africa, Uganda, Zambia and Zimbabwe (starting from 10%-58% for the 13 nations).

Kenya is main at 58% cell cash account penetration, with Somalia, Tanzania and Uganda “following intently” reporting round 35%. Namibia out of 13 nations has the least of cell cash penetration of about 10% (nonetheless increased than all others on this planet besides the opposite 12 African nations). Cell cash account is recorded to be widespread in East Africa (20% and 10% of adults have cell cash accounts and cell cash account solely respectively) than some other area.

Corporations offering monetary providers, be it providers or infrastructure is a very powerful and distinctive set of stakeholders who needs to be inspired to take the lead roles in monetary inclusion actions and implementations. Monetary providers companies are uniquely positioned, to make use of their present infrastructure and leverage to creating entry, and utilization of digital monetary providers.

They achieve this successfully and at a lesser price as in comparison with authorities businesses as a result of they’ll achieve this by their already present departments because the advertising and marketing and customer support departments. Monetary providers companies are driving innovation for digital finance throughout the globe. Corporations as GCAP have been investing in options to speed up monetary inclusion. It introduced that in its name for proposals on progressive digital expertise with enormous potential to advancing the monetary inclusion drive in sub-Saharan Africa, out of the over 200 candidates and proposals submitted, Monetary Expertise (Fintech) companies submitted (56%), Monetary Providers Suppliers (18%), Non-Governmental Organizations (NGOs) (13%) and Expertise Providers Suppliers (9%).

Rising proof from different comparable calls suggests that there’s a pattern, that the journey of utilizing progressive expertise and monetary inclusion within the sub-Saharan African shouldn’t be solely choosing up however even reveals a relatively promising outlook for the long run, the alternatives for nations within the area are monumental for nations in advancing monetary inclusion.

The decision now could be for nations at their coverage ranges to place themselves, armed with insurance policies and willingness of governments to help and collaborate with the personal sector to drive monetary inclusion actions. Nevertheless, to additional improve monetary and financial for significantly better achieve is a continues course of and doesn’t take only a few days however undoubtedly with out collaborations between public-private position and resolution institution and help, it’s going to take us relatively too lengthy. Collaboration is subsequently vital for monetary inclusion drives and actions.

For governments or the general public sector, their help in creating the wanted supportive framework and rules for the trade is vital. Rules and setting that helps innovation and drives whiles buyer rights are supported are a lot wanted on this sector. In offering help and serving to in creating an setting for monetary inclusion actions to make the required impacting results, authorities insurance policies will need to have some stability of care. By doing so, any coverage by a authorities on monetary inclusion that doesn’t take views from different vital stakeholders could also be carried out finally, however not with out difficulties and in some case unreasonable delay in implementation.

This may be attributed to quite a lot of causes: extra importantly, insurance policies could also be concluded, but when Monetary providers suppliers usually are not prepared or not in a position to implement these insurance policies, then, issues of “distressed“ insurance policies then start to indicate. In monetary inclusion drives, success relies upon totally on collaborations for enchancment between the public-private sectors.

The Alternatives for sub-Saharan African Economies

The alternatives exist for teams of people that want entry and utilization of monetary providers but unable due to the boundaries they confront principally. Sub-Saharan African governments and personal stakeholders can enhance on the regulatory constraints and permit for the faucet in expertise innovation respectively to design options that may open entry and utilization of monetary providers

An vital Phase of organized teams often out of the formal monetary financial system thus, the “Financial savings Teams” all the time have their frequent values and beliefs most frequently deeply rooted with cultural and social entrenchment that should be thought-about when focusing on with monetary inclusion merchandise and designs.

The teams often frequent in Asia, sub-Saharan Africa and Latin American come collectively for social and financial advantages and helps. They’ve totally different particular goals however generally amongst causes are for group financial savings, group insurance coverage, good buying and selling and every kind of group help techniques. At greatest design of product and providers for “financial savings teams” if the highest is efficiently accepted can solely be by a consultative course of, typically custom-made or tailored providers (most acceptable the place doable) and profitable the real curiosity of the teams.

There are over 14 million members of “Financial savings Teams” throughout 75 nations in sub-Saharan Africa, Asia and Latin America, representing a promising platform for monetary inclusion in under-served markets. Financial savings Teams provide an entry level for monetary service suppliers to remoted communities; they’re organized, expertise and disciplined; they combination demand throughout many low-income purchasers, and so they have recognized wants that monetary service suppliers can deal with. Additionally, these teams are very objective oriented and purposeful however lack sure monetary services- Some fundamental wants like accounts and funds and others refined wants like saving platforms. Tailoring merchandise to satisfy these segments who lack entry to some monetary providers and are in want of these monetary providers would create alternatives for monetary inclusiveness.

Prioritization of digital funds is a technique of minimizing corruption inside expenditures, be it the personal or public sector. Digitizing funds means higher monitoring of data of funds all through the worth chain of spending and transfers. Within the Agriculture financial system, it implies that when the federal government pays 1 million {dollars} ($1.000.000.00) immediately by “cell cash` to its citizenry for items and providers, then its almost definitely that, topic to price of the transaction, farmers will obtain their funds intact and identical. The susceptible citizen would then have worth for cash in coping with the federal government whiles having to profit from the alternatives that having an account and utilizing it comes with. Such shouldn’t be the case when bodily money modifications palms in funds.

The adoption stage of digital monetary inclusion with cell cash is usually excessive for sub-Saharan African. Stakeholders within the Public within the area can leverage its robust basis and utility of cell cash providers to scale up using digital funds, however programs they should be the backing infrastructure to develop entry as nicely. Improve in account possession as a foremost monetary inclusion indicator has primarily been by monetary establishments besides these recorded in Africa the place cell cash accounts drove the expansion in accounts possession from 24% to 34% in 2011 and 2014 respectively.

An space Africa is making large strides – Cell cash account penetration. Accounts possession and its definition have modified over simply three years when International Findex Database launched its first information for comparable indicators amongst nations on monetary inclusion. In 2014 it thought-about cell cash accounts as acknowledged accounts of their proper, hitherto in 2011 that wasn’t the case. The other was relatively the accepted case, and rightly so. At the moment the digital disruptions within the monetary, telecommunication and financial enviornment are having is impacts.

For policymakers and personal sector stakeholders, extra keenly vital is the truth that 5 of the 13 sub-Saharan African nations (The one 5 on this planet) – Somalia, Uganda, Côte d’Ivoire, Tanzania and Zimbabwe have an grownup inhabitants with extra cell account than they’ve from a proper conventional monetary establishment. What this implies is that, in these 5 nations, an peculiar man on the road is extra prone to have, use, belief and save in a cell cash account or pockets than saving with a conventional formal checking account. This comes with monumental alternatives and breakthroughs. Digital funds are snug, quick and cheaper than bodily money funds platforms.

Tailoring merchandise to satisfy these segments who lack entry to some monetary providers and are in want of these monetary providers would create alternatives for monetary inclusiveness. Prioritization of digital funds is a technique of minimizing corruption inside expenditures, be it the personal or public sector. Digitizing funds means higher monitoring of data of funds all through the worth chain of spending and transfers. Within the Agriculture financial system, it implies that when the federal government pays 1 million {dollars} ($1.000.000.00) immediately by “cell cash` to its citizenry for items and providers, then its almost definitely that, topic to price of the transaction, farmers will obtain their funds intact and identical. The susceptible citizen would then have worth for cash in coping with the federal government whiles having to profit from the alternatives that having an account and utilizing it comes with. Such shouldn’t be the case when bodily money modifications palms in funds

The adoption stage of digital monetary inclusion with cell cash is usually excessive for sub-Saharan African. Stakeholders within the Public within the area can leverage its robust basis and utility of cell cash providers to scale up using digital funds, however programs they should be the backing infrastructure to develop entry as nicely. Improve in account possession as a foremost monetary inclusion indicator has primarily been by monetary establishments besides these recorded in Africa the place cell cash accounts drove the expansion in accounts possession from 24% to 34% in 2011 and 2014 respectively.

An space Africa is making large strides – Cell cash account penetration. Accounts possession and its definition have modified over simply three years when International Findex Database launched its first information for comparable indicators amongst nations on monetary inclusion. In 2014 it thought-about cell cash accounts as acknowledged accounts of their proper, hitherto in 2011 that wasn’t the case. The other was relatively the accepted case, and rightly so.

At the moment the digital disruptions within the monetary, telecommunication and financial enviornment are having is impacts. For policymakers and personal sector stakeholders, extra keenly vital is the truth that 5 of the 13 sub-Saharan African nations (The one 5 on this planet) – Somalia, Uganda, Côte d’Ivoire, Tanzania and Zimbabwe have an grownup inhabitants with extra cell account than they’ve from a proper conventional monetary establishment. What this implies is that, in these 5 nations, an peculiar man on the road is extra prone to have, use, belief and save in a cell cash account or pockets than saving with a conventional formal checking account. This comes with monumental alternatives and breakthroughs. Digital funds are snug, quick and cheaper than bodily money funds

Suggestions

1) Regional and sub-regional our bodies in sub-Saharan Africa ought to take up the monetary inclusion drive as a precedence and guarantee peer-to-peer commitments of its members based mostly on particular person nation socio-economic dynamics.

2) Every sub-Saharan African nation ought to develop a Nationwide Monetary Inclusion Technique in a extremely consultative method at their nation ranges to information their efforts.

3) Sub-Saharan African governments ought to repeatedly help ongoing literature and analysis work on Monetary and Financial inclusion to supply dependable information will information the policymakers developmental aspirations and financial insurance policies. Due to this fact nations ought to arrange Monetary Inclusion Analysis Fund as a part of their Nationwide Monetary Inclusion Technique to help continues analysis on monetary inclusion points for his or her jurisdiction.

4) Sub-Saharan African International locations ought to commit a proportion (no less than 1%) of their annual GDP because the finances for Revolutionary expertise for the help of the digital financial system stimulus for sectors like monetary service and different industries to carry out.

5) Efforts needs to be made at nation and regional ranges to make using monetary providers delivered electronically cheaper – greatest apply is Wechat and AliPay fee options in China. Wechat particularly has no price construct up to be used of its platform for fee of products and providers, subsequently selling using cellphones and customers can switch money and make purchases digitally for items costing as little as half a greenback. It’s virtually doable to pay for an merchandise purchased at an quantity which is lower than a greenback with no further price besides the price of merchandise solely. These are among the readily felt advantages of Innovation Expertise throughout the banking area.

6) African authorities arrange help funding funds and accomplice companies which might design progressive applied sciences within the space.

[ad_2]

Source by Mark Yama Tampuri Jnr

{kind=link}